Interest on a car loan is the cost you pay to borrow money to purchase a vehicle, calculated as a percentage of your loan balance over time. Understanding how interest on car loans works and how it’s calculated can help you save thousands over the life of your loan.

So if you’re interested in having Jeopardy-champ-level knowledge of auto loan interest, we’ve got you covered!

In this post, we’ll answer frequently asked questions like:

- How does interest work on a car loan?

- How does auto loan interest work over time?

- How is interest calculated on a car loan?

- When do you pay the interest on a car loan?

- What affects your auto loan interest rate?

Key Takeaways:

- Car loan interest is the cost of borrowing, calculated on your remaining balance.

- Most auto loans use simple interest, not compound interest.

- Lower rates and shorter terms reduce total cost, even if payments are higher.

- Interest is front-loaded, so early payments matter most.

- Rates vary by credit, term, and lender, making comparison essential.

- Credit unions often offer lower rates and fewer fees than other lenders.

Interest on Car Loans — What Is It?

When you can’t or don’t want to buy your vehicle outright, you’ll need to finance the portion of the cost that you aren’t paying at the time of the purchase. The portion of the car’s value that you finance is your car loan.

As generous as your auto loan lender may be, they’re probably not going to let you borrow that chunk of money for an extended period of time for free. You pay a premium for the privilege of accessing and using those funds. That amount is the interest, usually expressed as a percentage, i.e., your interest rate.

It’s a tradeoff:

- The lender earns revenue for taking on risk.

- You get to drive away in a car without paying the full cost upfront.

At its core, this is how auto loan interest works.

How Do Car Loan Interest Rates Work?

A lot goes into determining your auto loan interest rate. Rates are influenced by a mix of economic conditions, lender policies, and borrower-specific factors, including:

- The market: Interest rates fluctuate based on the broader economy.

- The lender: Banks, dealerships, and credit unions all price loans differently.

- Loan length: Longer loans typically come with higher interest rates.

- Loan amount: Smaller loans may carry higher rates.

- The vehicle: Used cars often have higher rates than new cars.

- You: Your credit profile plays a major role. Strong credit typically means more favorable rates.

A savvy borrower keeps an eye on current average rates and evaluates their own credit standing. It’s always helpful to discuss your personal financial landscape and goals with a loan specialist — here at Valley Credit Union, we’re always happy to help!

You can also consider:

Related: Do I Need An Auto Loan Cosigner? [Everything You Need To Know]

What’s the Difference Between Interest Rate and APR?

One common source of confusion when comparing loans is the difference between interest rate and APR (Annual Percentage Rate).

- Interest rate reflects the cost of borrowing the principal.

- APR includes the interest rate plus certain fees associated with the loan.

APR gives you a more complete picture of the true cost of borrowing and is often the better number to compare when shopping between lenders. Credit unions frequently offer competitive APRs because they tend to charge fewer and lower fees than traditional banks or dealer financing.

How Is Interest Calculated on a Car Loan?

Most car loans use simple interest, not compound interest. This means interest is calculated only on the remaining principal balance, or the portion of the loan you still owe. You don’t pay interest on previously accrued interest.

So, how does interest work on a car loan in practice? As you make payments and reduce your principal balance, the amount of interest charged each month decreases.

Perhaps the easiest way to illustrate this is through an example.

Let’s walk through some numbers:

- Price of car: $30,000

- Amount of down payment (10%): $3,000

- Remaining amount you need to get a loan for: $27,000

The tables below show how different interest rates and loan terms affect monthly payments and total loan cost.

Loan Amounts by Interest Rate

| Interest Rate |

Terms (Years) |

Monthly Payment |

Total Interest Paid |

Total Cost of Loan |

| 3% |

3 |

$785.19 |

$1,266.94 |

$28,266.94 |

| 3% |

5 |

$485.15 |

$2,109.28 |

$29,109.28 |

| 3% |

7 |

$356.76 |

$2,967.76 |

$29,967.76 |

| 4% |

3 |

$797.15 |

$1,697.31 |

$28,697.31 |

| 4% |

5 |

$497.25 |

$2,834.77 |

$29,834.77 |

| 4% |

7 |

$369.06 |

$4,000.85 |

$31,000.85 |

| 5% |

3 |

$809.21 |

$2,131.71 |

$29,131.71 |

| 5% |

5 |

$509.52 |

$3,571.40 |

$30,571.40 |

| 5% |

7 |

$381.62 |

$5,055.71 |

$32,055.71 |

Loan Amounts by Term

| Interest Rate |

Terms (Years) |

Monthly Payment |

Total Interest Paid |

Total Cost of Loan |

| 3% |

3 |

$785.19 |

$1,266.94 |

$28,266.94 |

| 4% |

3 |

$797.15 |

$1,697.31 |

$28,697.31 |

| 5% |

3 |

$809.21 |

$2,131.71 |

$29,131.71 |

| 3% |

5 |

$485.15 |

$2,109.28 |

$29,109.28 |

| 4% |

5 |

$497.25 |

$2,834.77 |

$29,834.77 |

| 5% |

5 |

$509.52 |

$3,571.40 |

$30,571.40 |

| 3% |

7 |

$356.76 |

$2,967.76 |

$29,967.76 |

| 4% |

7 |

$369.06 |

$4,000.85 |

$31,000.85 |

| 5% |

7 |

$381.62 |

$5,055.71 |

$32,055.71 |

As you can see, at a given rate, a longer-term auto loan will have lower monthly payments, but will significantly increase the total interest paid. You’ll also notice that the monthly payments, at different rates over a given timeframe, may not be radically different.

Want to see what loan costs might look like for you? Skip the math and try out our handy Loan Calculator! Be sure to review the View Report tab. It breaks everything down clearly so you can see the progression over time.

What About Precomputed Loans?

Another type of loan you may encounter is a precomputed loan. This less-common structure calculates the total interest upfront and adds it to the loan balance, then divides that total evenly across payments.

Because interest is pre-set, paying off the loan early may not reduce interest as much as with simple-interest loans. This is one reason simple-interest auto loans, commonly offered by credit unions, are often more borrower-friendly.

When Do You Pay Car Loan Interest?

You pay interest throughout the life of your loan. Each monthly payment includes some portion that’s allocated to cover interest.

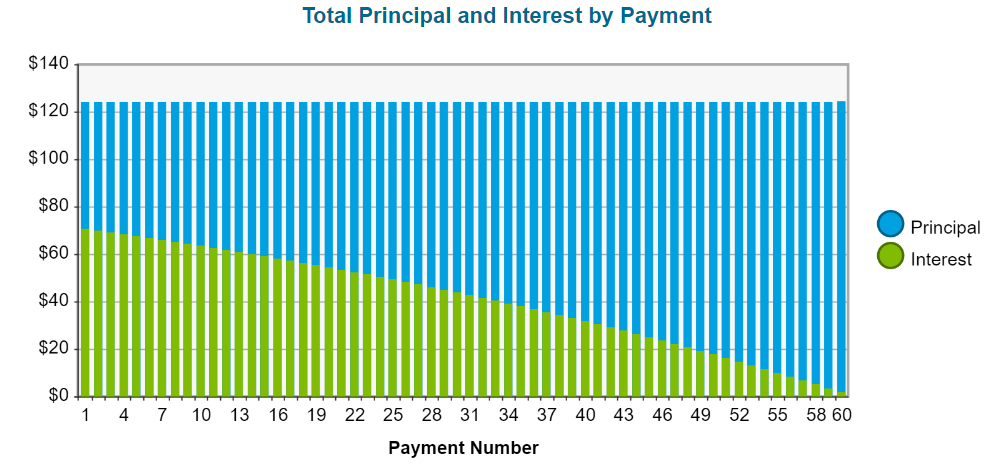

Unless otherwise stated, interest on a car loan is front-loaded. This means that you’re mostly paying down the interest obligation first before you ever start making serious headway on the loan principal.

Every payment you make reduces the balance owed on the principal of the loan to some degree. So you will see the interest portion of each payment diminish over time. Again, refer to that View Report tab on the Loan Calculator for a visualization of this in action. If you look closely, you’ll see the trendline isn’t straight — it bows.

Below is an exaggerated example (a $5,000 loan at 17% for 5 years) to make this pattern easier to see.

There are tactics you can use to chip away at the principal faster or to secure better rates over the course of your loan, though. We go into extreme detail in How to Pay Off Your Car Loan More Quickly. This is good info to have, whether you’re still shopping around for a loan or you are considering refinancing an existing auto loan.

How Your Credit Score Affects Auto Loan Interest

Your credit score plays a major role in determining your interest rate.

In general:

- Higher credit scores = lower interest rates

- Lower scores = higher borrowing costs

This can be seen very clearly by looking at national average auto loan rates. With a credit score of 781 or higher, the average auto loan rate for a new car is 4.88%, while for a credit score between 661 and 780, the average rate is 6.51%.

Even a one-point difference in interest can add up to thousands of dollars over the life of a loan. Credit unions often take a more holistic view of a borrower’s financial picture, which can help members with strong overall profiles—even if their credit isn’t perfect.

Related: Why a Credit Union May Have Better Car Loan Rates than a Dealer

FAQs About Car Loan Interest

Which lenders offer the best auto loan rates?

There are several options for financing your car, including:

- Dealership financing: Convenient, but rates may include markups.

- Banks: Often rigid underwriting and higher fees.

- Credit unions: Member-focused pricing, lower fees, and competitive rates.

Financing through a credit union often means paying less interest overall and having more flexibility if your situation changes.

Can you reduce the car loan interest you pay?

Yes. There are several strategies to lower total interest costs:

- Make extra principal payments early

- Choose a shorter loan term when possible

- Refinance if your credit improves or rates drop

Is car loan interest tax deductible?

Generally, no, unless the vehicle is used for qualified business purposes.

Does refinancing reset interest?

Refinancing replaces your existing loan with a new one, ideally at a lower rate or better term.

Do used cars always have higher interest rates?

Often yes, but strong credit and credit union financing can narrow the gap.

Is a longer loan ever a good idea?

It can be if it improves cash flow, but it usually increases total interest paid.

What is the advantage of financing through a credit union?

Members consistently choose credit unions because they offer:

- Lower rates

- Easier approvals

- Flexible terms

- Fewer fees

- Better tools and support

For even deeper looks at the pros of credit union vehicle financing, check out Why a Credit Union May Have Better Car Loan Rates than a Dealer and Why You Should Get Your Auto Loan From a Credit Union.

Because There’s More to Loans than Just Interest

Car loan interest is just one piece of vehicle financing. If you want to take a scenic drive through our knowledge base, we recommend making pit stops with these articles:

Working with Valley Credit Union… It’s in Your Best Interest

Our caring team is invested in your financial well-being. We’ll go out of our way to help you get the right auto loan for your situation. It’s our pleasure to guide you throughout the process and answer any questions you have.

In fact, it’s this dedication and knowledge that keep members coming back for all their banking needs. Feel free to reach out any time if we can be of assistance.

About the Author

Justin Roberts, Vice President of Lending

Justin Roberts, Vice President of Lending

Justin Roberts is our Vice President of Lending and has been in the financial industry for over 18 years. He is an Oregon State University Graduate and has just completed Western CUNA Management School. When he is not focused on helping the members at Valley, you will find him coaching his two sons and volunteering his time to help develop the youth in our communities through sports.